|

Forecast Period

|

2026-2030

|

|

Market Size (2024)

|

USD 12.18 Billion

|

|

CAGR (2025-2030)

|

13.5%

|

|

Fastest Growing Segment

|

Residential

|

|

Largest Market

|

North

|

|

Market Size (2030)

|

USD 26.03 Billion

|

Market Overview

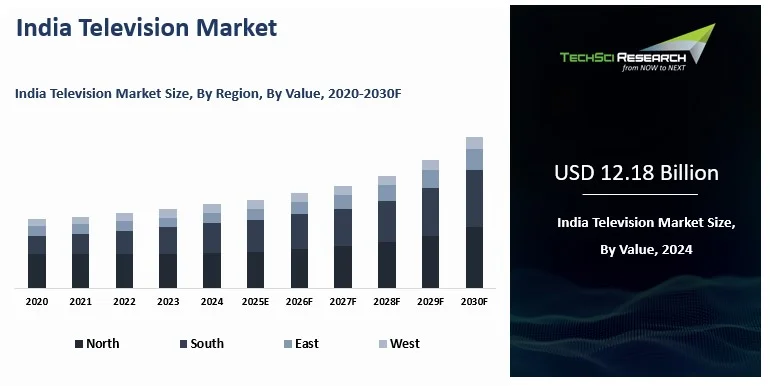

India Television Market was valued at USD 12.18 Billion in 2024 and is anticipated to reach USD 26.03 Billion by 2030, with a CAGR of 13.5% during 2025-2030. Television sets, commonly known as TVs, are electronic devices that showcase moving images and sound by receiving broadcast signals via a tuner and projecting them onto a screen. Initially bulky and CRT-based, TVs have evolved significantly with the adoption of LCD technology, becoming slimmer and lighter.

The television market is extensive, with TVs being a household essential. It has transitioned from being dominated by CRT to LCD screens, and newer technologies such as OLED are gaining prominence. According to the International Data Corporation (IDC) Quarterly Smart Home Devices Tracker, India saw shipments of 4.5 million televisions in the first half of 2023, marking an 8% increase compared to the previous year. This growth was driven by frequent sales events by e-commerce platforms, extensive new product launches and model updates by manufacturers, and the clearance of older inventory through various channels ahead of the festive season.

The online channel witnessed significant expansion, capturing a 25% increase year-over-year in the first half of 2023, achieving a 39% television market share in India driven by online sales festivals. Although 32-inch and 43-inch screens remain popular, collectively holding a 71% market share, larger screen sizes are gaining traction. The share of 55-inch screens increased to 12% from 9% a year ago in the first half of 2023, contributing to a 35% year-on-year growth in the USD$400+ price segment.

Despite stable sales figures, the market continues to innovate, particularly with advancements in smart TV functionalities and seamless integration with streaming services. According to some studies, the media and entertainment sector, including television, is projected to achieve a market size of USD 100 billion by 2030. In India, the media and entertainment industry has surpassed USD 27.56 Billion, with television accounting for 30%. Despite television maintaining its status as the largest contributor historically, digital media is anticipated to surpass it in the near future. While overall TV viewing time has seen a modest increase of 2%, there has been a slight decline of 1% in affluent audiences' TV consumption. This decrease has been offset by a 4% rise in TV viewing among lower-income audiences, influencing shifts in the television market share in India across different consumer segments.

Download Free Sample Report

Key Market Drivers

Rising Disposable Incomes and Urbanization

India's economic growth has led to a substantial increase in disposable incomes among its population. According to the People's Research on India's Consumer Economy (PRICE), India's middle class stood at 43.2 crore in 2021 and is projected to reach 102 crore by 2047, constituting approximately 61% of the total population. The average annual household disposable income is set to rise to approximately ₹20 lakh at 2020-21 prices by 2047. India's household consumption has doubled over the past decade, reaching $2.1 trillion in 2023, positioning the country to become the world's third-largest consumer market. As more households move into the middle and upper-income brackets, there is a greater propensity to spend on consumer electronics, including televisions.

Urbanization, with more people living in cities and towns, also plays a crucial role. Projections indicate that by 2047, more than 50% of India's population will be living in urban areas, with cities like Indore, Jaipur, and Coimbatore witnessing increased development due to better infrastructure and job opportunities. Urban areas typically have higher television penetration rates due to better infrastructure, higher media consumption, and greater exposure to new technologies. These factors collectively contribute to the evolving TV market share in India, as brands compete to meet the rising expectations of urban consumers.

The increase in disposable incomes and urbanization has propelled the demand for larger screen sizes, higher resolution displays, and advanced features in televisions. Consumers are now more inclined towards purchasing smart TVs that offer internet connectivity, streaming services, and interactive features. India's active connected TV (CTV) user base has reached approximately 129.2 million, translating to an estimated 35 to 40 million CTV homes, with CTV penetration growing by 87% within a single year. Major brands such as Samsung, LG, Sony, Xiaomi, OnePlus, Realme, Haier, TCL, and Vu are actively competing in the Indian smart TV segment. As urbanization progresses and consumer aspirations for better viewing experiences grow, these shifts will continue to reshape the TV market share in India, influencing product innovation, pricing strategies, and distribution models across both traditional retail and online platforms.

Technological Advancements and Product Innovation

Technological advancements have been pivotal in shaping the television market in India. The transition from traditional CRT (cathode-ray tube) to modern LCD (liquid crystal display) and LED (light-emitting diode) screens has significantly improved picture quality, reduced power consumption, and enabled thinner designs. The introduction of OLED (organic light-emitting diode) and QLED (quantum dot LED) technologies has further enhanced viewing experiences with deeper blacks, brighter colors, and better contrast ratios. In May 2025, Samsung launched its ultra-premium 2025 models of Neo QLED 8K, Neo QLED 4K, OLED, QLED TVs, and The Frame lineup with Samsung Vision AI technology for Indian consumers. In May 2024, Sony India introduced the BRAVIA 2 Series featuring 4K Ultra HD LED display technology with Google TV integration.

Product innovation has also driven market growth. Manufacturers continually introduce new features such as HDR (high dynamic range), higher refresh rates, and improved sound systems to cater to consumer demands for immersive home entertainment experiences. LG's OLED TVs feature Dolby Vision IQ and Dolby Atmos with α9 AI Processor 4K Gen7 for enhanced picture and sound quality. Smart TVs, equipped with built-in Wi-Fi, app stores, voice control, and compatibility with streaming services like Netflix and Amazon Prime Video, have become increasingly popular among tech-savvy consumers. Emerging trends include integration of AI-based voice assistants, smart home compatibility, Android and WebOS-based smart interfaces, screen casting, personalized content recommendations, and low-latency gaming features.

Increasing Demand for Content and Entertainment

The demand for diverse and high-quality content has been a significant driver of the television market in India. With the proliferation of digital streaming platforms, OTT (over-the-top) services, and satellite TV providers, consumers have access to a vast array of entertainment options. India now has over 600 million OTT users, representing approximately 41% of the country's population. JioHotstar has reached 300 million subscribers as of June 2025, approaching Netflix's global subscriber count of 301.63 million, with the 2025 IPL digital audience reaching 652 million viewers. Netflix entered India in 2016 and maintains 10 million users in the country, while Amazon Prime Video has approximately 20 million users. The availability of such varied content across multiple languages and genres has played a crucial role in boosting television sales in India, as consumers increasingly seek advanced TVs that can enhance their content consumption experience.

The COVID-19 pandemic further accelerated this trend as people spent more time at home, leading to increased consumption of digital content on televisions. This shift in viewing habits has underscored the importance of having a quality television with enhanced audio-visual capabilities. Indian content is experiencing unprecedented global reach through streaming platforms, with nearly 25% of total viewership for Indian OTT and digital programming now originating from overseas markets. The total number of active paid OTT subscriptions in India is estimated at 148.2 million, including subscriptions through telecom bundles and OTT aggregators. As content providers continue to invest in producing original and exclusive content, there is a corresponding demand for televisions that can deliver an immersive and cinematic experience at home further contributing to the steady rise in television sales in India across both urban and semi-urban markets.

Government Initiatives and Regulatory Policies

Government initiatives and regulatory policies also influence the television market in India. Programs such as Digital India and Make in India promote domestic manufacturing, thereby boosting the production of televisions within the country. The Production Linked Incentive (PLI) Scheme, with an incentive outlay of ₹1.97 lakh crore covering 14 strategic sectors, powers Digital India by driving local production of electronics, making technology more accessible and affordable. In March 2025, the Indian Cabinet approved a ₹22,919 crore PLI scheme for non-semiconductor electronics components, including display modules, to build a domestic component ecosystem. The India Semiconductor Mission, backed by a ₹76,000 crore package, aims to support investments in semiconductor fabrication, display manufacturing, and chip design. This has led to increased availability of affordable TVs for consumers across different income segments.

Regulatory frameworks, such as the implementation of the Goods and Services Tax (GST), impact pricing and market dynamics. Following the 56th GST Council Meeting in September 2025, a uniform 18% GST is now applicable on all television sizes, including LED TVs larger than 32 inches, which were previously subject to 28% GST. LCD/LED TV open cell components are now fully exempt from customs duty, encouraging local assembly and production. These reductions in import duties on key components used in television manufacturing have contributed to lower prices and improved availability of technologically advanced models.

Key Market Challenges

Price Sensitivity and Affordability

Price sensitivity is a significant challenge in the Indian television market, particularly in a country where a large portion of the population belongs to middle and lower-income groups. While the demand for televisions with advanced features like smart capabilities and high-definition displays is increasing, affordability remains a critical factor. Basic 32-inch HD Smart LED TVs are available starting from ₹15,000, while 43-inch 4K Ultra HD Smart TVs range from ₹33,000 to ₹39,000. In contrast, premium OLED televisions from brands like LG and Samsung range from ₹1,24,299 for a 48-inch model to over ₹15,66,999 for a 97-inch variant. Many consumers are constrained by budget limitations, which restrict their ability to purchase higher-end models with the latest technologies.

Manufacturers and retailers are continually pressured to offer competitive pricing while balancing the costs associated with importing components, technological upgrades, and distribution expenses. This challenge is exacerbated by fluctuations in exchange rates, import duties, and regulatory policies that affect the final retail prices of televisions.

Diverse Consumer Preferences and Regional Variances

India is a diverse country with varied consumer preferences and regional differences. Preferences for screen sizes, features, and brands can vary significantly across different states and cities. According to Bain & Company research, in the North, brands are often associated with status, while in the South, shoppers view brands as markers of quality, manifesting in more branded searches in electronics. While urban areas generally exhibit higher demand for larger screen sizes and smart TVs, rural markets may prioritize affordability and basic functionality. Rural TV penetration stands at approximately 61% of total rural households, compared to significantly higher rates in urban areas.

Navigating these diverse preferences requires tailored marketing strategies, localized product offerings, and distribution channels that cater to specific regional requirements. By 2029, Tier 2 and Tier 3 cities are expected to see over 25 million square feet of new retail space, with the northern region accounting for 44% of upcoming retail supply and the southern region contributing 30%. Growth of premium products and high-ticket items in smaller towns is 5-7 percentage points higher than urban areas due to the availability of finance. This complexity adds operational challenges for manufacturers and retailers seeking to penetrate and expand their market share across diverse demographic and geographic segments.

Intense Competition and Market Saturation

The television market in India is highly competitive, characterized by the presence of both domestic and international brands offering a wide range of products across various price points. Established players like Samsung, LG, Sony, and Panasonic compete with emerging brands and local manufacturers vying for market dominance. The Indian smart TV market features major players including Samsung Electronics, Sony India, LG Electronics India, Xiaomi, OnePlus, Realme, Haier, TCL, Vu Televisions, and Thomson. In 2024, Samsung India overtook Xiaomi to become the top smart TV brand in India, while LG follows closely behind. LG and Samsung emerged as growth leaders in 2024, while the collective "others" category still holds a significant 40% share of the overall market, underscoring a competitive niche environment.

Intense competition contributes to price wars, reducing profit margins for manufacturers and limiting opportunities for new entrants to gain traction. Market saturation in urban areas, where television penetration rates are relatively high, further intensifies competition as brands strive to differentiate themselves through innovation, product quality, and after-sales service.

Technological Obsolescence and Rapid Advancements

Technological obsolescence poses a challenge for both consumers and manufacturers in the television market. The rapid pace of technological advancements, such as the transition from LCD to OLED screens or the integration of AI-driven smart features, can render older models obsolete within a short span of time. Samsung launched its 2025 Neo QLED 8K, Neo QLED 4K, OLED, QLED TVs with Samsung Vision AI technology in May 2025, while LG introduced its evo AI G5 and C5 series with α9 AI Processor 4K Gen7. Sony continues to innovate with its BRAVIA XR Master Series featuring cognitive processor technology.

Consumers often face the dilemma of choosing between investing in new technologies that promise enhanced viewing experiences and sticking with existing models that may become outdated. Manufacturers, on the other hand, must continually innovate and upgrade their product offerings to stay competitive and meet evolving consumer expectations.

Infrastructure and Connectivity Issues

Infrastructure and connectivity challenges in certain parts of India, particularly in rural and remote areas, present obstacles to the adoption of advanced television technologies. According to the Ministry of Power, average electricity supply in rural areas has increased from 12.5 hours in 2014 to 22.6 hours in 2025, while urban areas receive 23.4 hours of supply. Under the SAUBHAGYA Scheme, 2.86 crore households have been electrified, and an additional 6.84 lakh unelectrified households have been sanctioned under the Revamped Distribution Sector Scheme (RDSS). The government has invested ₹1.85 lakh crore in distribution infrastructure strengthening under DDUGJY/IPDS/SAUBHAGYA schemes, adding 2,927 new sub-stations and installing 6,92,200 distribution transformers.

On connectivity, as of March 2024, 6.12 lakh villages out of 6.44 lakh have 3G/4G mobile connectivity, meaning 95.15% of villages have internet access. Out of India's 954.40 million internet subscribers, 398.35 million are rural subscribers. Under BharatNet, 2.13 lakh Gram Panchayats have been made service-ready, with plans to provide optical fibre connectivity to 42,000 uncovered GPs and 3.84 lakh villages on a demand basis, along with 1.5 crore rural home fibre connections. Improving connectivity and accessibility to digital services are essential for expanding the reach of television manufacturers and ensuring equitable access to modern entertainment technologies across the country.

Key Market Trends

Shift

towards Larger Screen Sizes and Higher Resolutions

One of the prominent trends in the

Indian television market is the increasing preference for larger screen sizes

and higher resolutions. As disposable incomes rise and consumers seek enhanced

viewing experiences, there is a growing demand for televisions with bigger

screens, such as 55 inches and above. Larger screens provide a more immersive

viewing experience, making them ideal for watching high-definition content,

sports events, and movies.

Simultaneously, there is a shift towards

higher resolution displays, particularly 4K Ultra HD and even 8K resolutions.

These technologies offer sharper images, vibrant colors, and better clarity,

catering to the discerning preferences of Indian consumers who prioritize

visual quality in their home entertainment setups.

Adoption

of Smart TVs and Connected Features

Smart TVs have gained significant

traction in the Indian market, driven by the increasing availability of

high-speed internet connectivity and the growing popularity of digital

streaming services. Smart TVs offer built-in Wi-Fi capabilities, app stores, and

compatibility with popular streaming platforms such as Netflix, Amazon Prime

Video, and Disney+ Hotstar.

Consumers are increasingly seeking

televisions that not only provide traditional broadcast content but also offer

a range of interactive features, voice control options, and access to a wide

array of on-demand content. This trend is reshaping viewing habits, as

households embrace the convenience of streaming their favorite shows, movies,

and live sports directly on their TV screens.

Rise

of OLED and QLED Technologies

OLED (organic light-emitting diode) and

QLED (quantum dot LED) technologies represent a significant advancement in

television displays, offering superior picture quality and enhanced viewing

experiences. OLED TVs, known for their deep blacks, rich colors, and wide

viewing angles, have garnered attention among consumers seeking premium viewing

experiences.

Similarly, QLED TVs utilize quantum dots

to enhance brightness levels, color accuracy, and overall image clarity. These

technologies are increasingly being integrated into high-end television models

offered by leading brands, catering to consumers' demands for superior visual

performance and advanced display technologies.

Expansion

of Content and Streaming Services

The expansion of digital content and

streaming services has transformed the television landscape in India. OTT

(over-the-top) platforms such as Netflix, Amazon Prime Video, Disney+ Hotstar,

and others have witnessed rapid growth, offering a diverse range of content

including original series, movies, documentaries, and live sports.

This trend has fueled the demand for

smart TVs capable of seamlessly accessing and streaming content from multiple

platforms. Manufacturers and content providers are forging partnerships and

licensing agreements to deliver exclusive content to smart TV users, enhancing

the appeal of these devices among tech-savvy consumers.

Emphasis

on Energy Efficiency and Sustainability

Energy efficiency and sustainability

have emerged as important considerations in the Indian television market. With

increasing awareness about environmental impact and energy consumption,

consumers are prioritizing energy-efficient models that comply with

international standards such as Energy Star ratings.

Manufacturers are responding by

developing televisions with advanced power-saving features, LED backlighting

systems, and eco-friendly materials. This trend not only appeals to

environmentally conscious consumers but also aligns with regulatory initiatives

aimed at reducing carbon footprints and promoting sustainable manufacturing

practices.

Segmental Insights

Screen

Size Insights

In the India Television Market, the

50''-59'' screen size segment has emerged as the dominant choice among

consumers. This segment appeals to a wide range of households seeking a balance

between screen size, viewing comfort, and affordability. Consumers are increasingly opting for larger

screen sizes within this range to enjoy an immersive viewing experience for

movies, sports, and gaming. The 50''-59'' category strikes a balance between

providing a cinematic feel while still being practical for most living room

sizes in urban and suburban homes across India.

Manufacturers have responded by offering

a diverse array of models in this segment, incorporating advanced technologies

such as 4K Ultra HD resolution, HDR (high dynamic range), and smart TV

capabilities. These features enhance the viewing experience by delivering

vibrant colors, sharp details, and seamless access to streaming content and

applications. Additionally, competitive pricing strategies and promotional

offers from leading brands and retailers have contributed to the popularity of

the 50''-59'' segment, making it a preferred choice for consumers looking to

upgrade their home entertainment setups without compromising on quality or

budget.

Distribution

Channel Insights

Supermarkets and hypermarkets have

emerged as the dominating distribution segment in the India television market.

These retail formats offer significant advantages such as wide product

selections, competitive pricing, and convenient shopping experiences,

attracting a large number of consumers looking to purchase televisions. One of

the key factors driving growth in supermarkets and hypermarkets is their

ability to showcase a diverse range of television brands and models under a

single roof. This allows consumers to compare features, screen sizes, prices,

and customer reviews before making a purchase decision. The availability of

knowledgeable staff and interactive displays further enhances the shopping

experience, helping consumers make informed choices based on their specific

preferences and requirements.

Moreover, supermarkets and hypermarkets

often run promotional campaigns, discounts, and bundled offers on televisions,

attracting price-sensitive consumers seeking value for money. These retail

formats also benefit from their strategic locations in urban and semi-urban

areas, catering to a wide demographic of consumers who prefer the convenience

of one-stop shopping for electronics. As consumer preferences evolve and demand

for televisions continues to grow, supermarkets and hypermarkets are poised to

play a pivotal role in shaping the distribution landscape of the Indian

television market, offering both accessibility and competitive pricing to meet

the diverse needs of consumers across the country.

Download Free Sample Report

Regional Insights

In the India Television Market, the

North region has emerged as the dominant and fastest-growing segment.

Comprising states such as Delhi, Uttar Pradesh, Rajasthan, Haryana, Punjab, and

others, the North region showcases robust growth in television sales driven by

several factors.

One of the primary reasons for the

dominance of the North region is its high population density and urbanization

rate. Metropolitan cities like Delhi and NCR (National Capital Region) have a

large concentration of affluent consumers with disposable incomes, who exhibit

a strong inclination towards purchasing consumer electronics, including

televisions. The presence of a burgeoning middle class also contributes

significantly to the demand for televisions in urban and semi-urban areas

across the region. Furthermore, the North region benefits from extensive retail

infrastructure, including modern retail chains, electronics stores, and

hypermarkets, which cater to the diverse preferences of consumers. These retail

outlets offer a wide range of television brands, sizes, and features, coupled

with competitive pricing and promotional offers, which attract consumers

seeking value and quality.

Additionally, the North region

experiences a high demand for smart TVs and advanced technologies due to

increasing digital literacy and connectivity. Consumers in urban centers are

keen on accessing streaming services, online content, and interactive features

offered by smart televisions, further driving the growth of this segment in the

North Indian market. Overall, the North region's dominance in the India

Television Market is underscored by its economic vibrancy, consumer preferences

for premium home entertainment experiences, and robust retail infrastructure,

making it a pivotal growth driver in the national television industry.

Recent Developments

- February 2024 — Reliance Industries (via Viacom18) and Walt Disney (via Star India) signed binding agreements to merge their India media assets, creating a joint venture valued at Rs 70,352 crore (~USD 8.5 billion), combining 120+ TV channels and two streaming services (JioCinema and Hotstar) to reach 750 million users.

- November 2024 — Reliance intimated the scheme of arrangement for the merger of Star Television Productions Ltd (STPL) with Star India (now JioStar India), with Star India's unsecured creditors unanimously approving the deal in December 2024.

- September 2025 — NCLT approved the merger of Star Television Productions with JioStar, with the transaction designed to simplify holding structure, optimize capital, and reduce costs.

- December 2025 — Reliance completed the merger of Star Television Productions with JioStar, marking finalization of the Reliance–Disney India media consolidation.

- January 2024 — Sony officially terminated the proposed Sony–Zee merger on January 22, 2024, citing unmet conditions after protracted negotiations and missed deadlines, ending plans for what would have been another major India TV/media consolidation.

- May 2025 — Sony India launched the BRAVIA 2 II series (4K Ultra HD LED with Google TV) in sizes from 43 to 75 inches, starting at Rs 50,990, featuring the X1 4K Processor and gaming enhancements.

- May 2025 — TCL launched its QD Mini-LED C6K and C6KS series alongside QLED P8K, P7K, and 4K HDR P6K TVs in India, with C6K starting at Rs 53,990, featuring AiPQ Engine, HVA panels, and Google TV integration.

- July 2025 — LG India unveiled its 2025 OLED evo (G5, C5, B5) and QNED evo TV lineup with Alpha 11 AI Processor Gen2, AI Magic Remote, and AI-powered features like AI Concierge and AI Voice ID; prices start at Rs 149,990 for OLED C5, going up to Rs 24,99,990 for the 97-inch G5.

- In 2024, LG, a South Korean technology

company, anticipates a 25-30% growth this year in response to the trend of

premiumization in India's TV market. Consumers in India are increasingly

interested in advanced technologies and larger screen sizes. To capitalize on

this demand and solidify its leading position in the Indian market, LG has

introduced a new lineup of AI-powered smart TVs. This Next Generation of AI TVs

includes 55 newly launched models, offering sizes ranging from 43 inches to 97

inches.

- In 2024, Samsung, has unveiled a new

generation of AI TVs with the launch of its ultra-premium Neo QLED 4K, Neo QLED

8K, and OLED TVs at the ‘Unbox & Discover’ event in Bengaluru. The 2024

lineup of TVs enhances home entertainment by integrating powerful AI-driven

solutions. Samsung is leveraging Artificial Intelligence (AI) to enhance

consumers’ lifestyles across various product categories. By integrating AI into

home entertainment, we aim to deliver exceptional viewing experiences for our

customers.

Key Market Players

- Samsung India Electronics Pvt Ltd.

- LG Electronics India Private Limited

- Xiaomi Technology India Private Limited

- Oneplus Technology India Private Limited

- Sony India Private Limited

- Hisense India Private Limited

- TCL-India Holdings Private Limited

- Intex Technologies (India) Limited

- Panasonic Life Solutions India Private

Limited

- Haier Appliances India Pvt Ltd

|

By Screen Size

|

By Display Type

|

By Distribution

Channel

|

By Region

|

- 39'' and Below

- 40''-49''

- 50''-59''

- Above 59''

|

|

- Multi-Branded Stores

- Supermarkets & Hypermarkets

- Online

- Exclusive Stores

- Others

|

|

Report Scope:

In this report, the India Television Market has

been segmented into the following categories, in addition to the industry

trends which have also been detailed below:

- India Television Market, By Screen

Size:

o 39'' and Below

o 40''-49''

o 50''-59''

o Above 59''

- India Television Market, By Display

Type:

o LED

o OLED

o Others

- India Television Market, By Distribution

Channel:

o Multi-Branded Stores

o Supermarkets & Hypermarkets

o Online

o Exclusive Stores

o Others

- India Television Market, By

Region:

o North

o South

o East

o West

Competitive Landscape

Company Profiles: Detailed analysis of the major companies presents

in the India Television Market.

Available Customizations:

India Television Market report with the given

market data, TechSci Research offers customizations according to a company's

specific needs. The following customization options are available for the

report:

Company Information

- Detailed analysis and

profiling of additional market players (up to five).

India Television

Market is an upcoming report to be released soon. If you wish an early delivery

of this report or want to confirm the date of release, please contact us at [email protected]