|

Forecast

Period

|

2026-2030

|

|

Market

Size (2024)

|

USD

961.21 Million

|

|

Market

Size (2030)

|

USD

1491.85 Million

|

|

CAGR

(2025-2030)

|

7.80%

|

|

Fastest

Growing Segment

|

ICSI

IVF

|

|

Largest

Market

|

West India

|

Market Overview

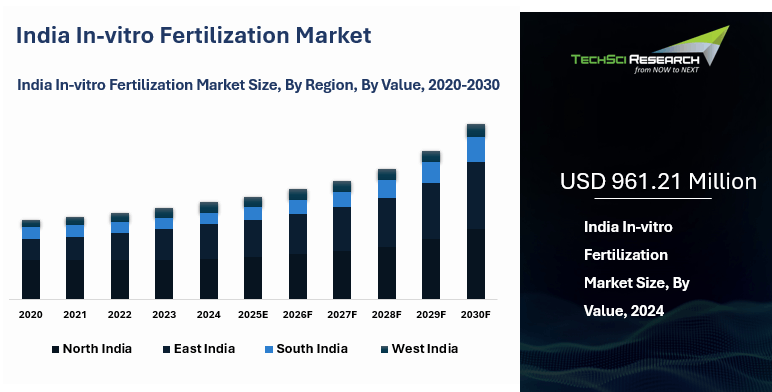

India’s In-vitro Fertilization (IVF) market was valued at USD 961.21 million in 2024 and is projected to reach USD 1,491.85 million by 2030, growing at a CAGR of 7.80% during the forecast period.

In vitro fertilization (IVF), a key assisted reproductive technology, has transformed infertility treatment by enabling fertilization outside the body and embryo implantation in the uterus. It offers hope to couples facing conditions such as blocked fallopian tubes or male infertility. In India, the IVF market is growing rapidly due to rising infertility rates, delayed marriages, lifestyle changes, and increasing awareness. Technological advancements like embryo freezing and genetic testing have improved success rates. Expanding fertility clinics, medical tourism, and supportive partnerships are boosting adoption. Despite cost and regulatory challenges, India’s IVF market is expected to witness sustained growth in the coming years.

Download Free Sample Report

Key Market Drivers

Growing Success Rate of IVF Technology

The growing success and standardization of in vitro fertilization technology are strengthening demand for fertility treatment in India, as better laboratory practices, controlled stimulation protocols, embryo culture systems, cryopreservation, and more structured clinical pathways are making assisted reproduction more credible and accessible for couples seeking formal infertility care.

Confidence in regulated treatment is also improving because the Assisted Reproductive Technology Regulation Act, 2021 requires clinics and banks to be registered under the national framework, while the government’s National ART and Surrogacy Registry functions as a public record system that allows patients and authorities to verify approved providers and track registration status more transparently.

This shift toward documented and quality-controlled care is further reinforced by the national registry’s expanding footprint, with the official registry showing 174 registered ART clinics and 136 registered ART banks on the publicly accessible lists, signaling steady formalization of India’s fertility ecosystem even as more providers continue entering the approval pipeline. Increased awareness, delayed childbearing, and reduced stigma are adding to utilization, but organized private networks are also playing a central role by widening access beyond major metros through larger multi-city delivery models supported by specialist staffing and technology-backed protocols.

For instance, Indira IVF says it operates 165 plus centres across more than 20 states, has a team of 340 plus IVF doctors, and has helped more than 1,75,000 couples pursue parenthood, illustrating how major fertility players are scaling standardized IVF services across India and reinforcing patient confidence in formal treatment pathways.

Increasing Awareness About IVF Technology

Rising awareness of IVF is a major factor fueling demand for fertility treatment in India, and that shift is becoming more visible as patients increasingly seek care through formal, regulated providers rather than informal or fragmented pathways. The policy environment is reinforcing this confidence because the National ART and Surrogacy Registry, hosted under the Ministry of Health and Family Welfare, functions as a public record system for ART clinics and banks, while the registry’s public lists show 174 registered ART clinics and 136 registered ART banks, making it easier for patients to identify approved providers and strengthening trust in standardized fertility care.

Social change is adding to this momentum, as UNFPA’s analysis of NFHS-5 shows the median age at first marriage among women aged 20 to 49 increased from 17.2 years in 2005–06 to 19.2 years in 2019–21, a pattern that aligns with later family formation and greater awareness of age-related fertility challenges. Large organized networks are also amplifying awareness through wider geographic reach, with Indira IVF stating that it operates more than 165 centres across over 20 states and has helped more than 1,75,000 couples pursue parenthood.

For instance, Yellow Fertility announced in 2025 that it plans to scale to 100 IVF centres by 2030, highlighting how rising public acceptance of fertility treatment is encouraging providers to expand beyond major metros into a broader national footprint.

Delayed Onset of Pregnancies

The delayed onset of pregnancies is becoming an important driver of IVF demand in India, as later marriages, longer education pathways, and career-focused life choices are pushing more couples to seek fertility support at ages when natural conception can become more difficult and clinically time sensitive. UNFPA’s analysis of NFHS-5 shows that the median age at first marriage among women aged 20 to 49 rose from 17.2 years in 2005–06 to 19.2 years in 2019–21, indicating a clear shift toward later family formation that aligns with rising awareness of age-related fertility challenges.

This social transition is strengthening the role of IVF as a practical and increasingly accepted option, especially as organized fertility networks expand technology-enabled care and improve patient confidence through wider access to specialist services.

Increasing Cases of Infertility

Rising infertility cases across India are fueling stronger demand for IVF, as the burden of infertility is becoming more visible across both urban and non-metro populations and is pushing more couples toward formal fertility evaluation and assisted reproductive treatment.

A recent national analysis reported infertility prevalence at 18.7 per 1,000 women among those married for at least five years and currently in union, while broader reviews note that infertility in India is influenced by delayed childbearing, lifestyle change, stress, obesity, smoking, environmental exposure, and uneven access to timely reproductive care.

This has made IVF increasingly relevant as a structured clinical solution, especially as advanced procedures such as ICSI, standardized laboratory protocols, and technology-supported fertility workflows help providers address a wider range of male and female infertility cases with greater confidence. Greater awareness through digital platforms and specialist-led counseling is also encouraging earlier treatment seeking, and the expansion of organized clinic networks is bringing fertility services closer to patients outside traditional metro hubs.

For instance, Indira IVF states that it operates 165 plus centres across more than 20 states with 340 plus IVF doctors and has helped over 1,75,000 couples pursue parenthood, showing how major fertility providers are scaling capacity to meet the country’s rising infertility-driven demand for IVF.

Key Market Challenges

Complications Associated with In-Vitro Fertilization

Although demand for IVF in India continues to rise, broader adoption is still moderated by patient concerns about treatment-related complications, especially multiple pregnancy and ovarian hyperstimulation syndrome, which make many couples more cautious before starting a cycle. Multiple pregnancy remains a key concern because the transfer of more than one embryo increases the likelihood of twins or higher-order pregnancies, and authoritative guidance notes that such pregnancies carry higher risks including miscarriage, high blood pressure, diabetes, prematurity, and other maternal and neonatal complications.

OHSS adds another layer of hesitation, as it is a potentially serious reaction to ovarian stimulation drugs that can range from mild to severe, and the risk may rise further when pregnancy occurs, particularly in multiple pregnancies. India’s regulatory framework is designed to reduce this apprehension through stronger counseling and clearer communication, since the ART law requires clinics to counsel patients on the chances of success as well as the advantages and disadvantages of procedures, while the 2022 rules also recognize the need to address psychological stress and unrealistic expectations.

Social Stigma, Ethical, and Legal Issues Associated with In-Vitro Fertilization

Social stigma, ethical debates, and regulatory complexity continue to influence IVF demand in India, because infertility is still viewed in many communities as a sensitive personal issue, causing some couples to delay treatment despite the growing availability of medically advanced fertility options.

Ethical hesitation also affects adoption, particularly around embryo handling, storage, and disposal, while concerns over multiple pregnancy and treatment transparency can make decision-making more difficult for patients. At the same time, India now has a more formal legal structure than before, as the Assisted Reproductive Technology Regulation Act, 2021 created a regulated framework and the National ART and Surrogacy Portal allows patients to identify registered providers more transparently, which helps reduce mistrust and improve confidence in structured fertility care.

Key Market Trends

Increasing Government Support

The Indian government is playing a central role in strengthening the in-vitro fertilization (IVF) market. Around 25 to 30 million couples in India face infertility, and policies aimed at expanding access to affordable reproductive care are driving growth.

Two landmark legislations, the Assisted Reproductive Technology (Regulation) Act, 2021, and the Surrogacy (Regulation) Act, 2021, have introduced strict ethical and safety standards. These laws have reinforced India’s reputation as a regulated and patient-friendly IVF destination.

Access to IVF is widening as government hospitals open specialized fertility centers, many offering subsidized or free services. Examples include:

- Goa Medical College and Hospital, which launched a free infertility treatment center in August 2023

- AIIMS Delhi, offering low-cost IVF treatment

- Lok Nayak Hospital, which opened Delhi’s first government-run IVF center

Affordability is further supported by Pradhan Mantri Bhartiya Jan Aushadhi Kendras (PMBJK), expected to expand to 10,500 centers by March 2025, providing low-cost fertility medicines. IVF treatment in India costs between USD 2,000 and 5,000 per cycle compared to USD 15,000 to 20,000 in the U.S. or Europe. This cost advantage positions India as a leading hub for reproductive tourism.

Government schemes such as the Production Linked Incentive (PLI) are also promoting local manufacturing of IVF drugs and devices, reducing import dependency. Public-Private Partnerships (PPPs) are channeling investment and expanding fertility services into Tier-II and Tier-III cities.

Emergence of Fertility Tourism

India is now a major destination for fertility treatments, with more than 2,500 clinics offering services like IVF, intracytoplasmic sperm injection (ICSI), egg donation, and advanced technologies, including AI-assisted embryo selection and improved cryopreservation.

Specialists in India combine technical expertise with patient-centered care, addressing the challenges of infertility that affect one in six couples worldwide. A major driver of international demand is cost. IVF treatment in India costs less per cycle compared to the U.S. and Canada, while maintaining success rates of 40-50% for younger women, consistent with global averages.

Fertility tourism is growing rapidly, with international patient inflow more than doubling in recent years and around 200,000 to 250,000 IVF cycles performed annually. India’s mix of affordability, advanced technology, and quality care continues to strengthen its standing as a global fertility hub.

Segmental Insights

Donor Insights

Based on donor,

in the year 2024, the segment of fresh non-donor IVF cycles emerged as the

dominant force in the India In-vitro Fertilization Market. This can be

attributed to the remarkable success rate associated with fresh non-donor IVF

cycles, which have shown consistent positive outcomes in helping couples

achieve their dream of parenthood. With their high success rate and the ease of

implantation they offer, fresh non-donor IVF cycles have become the preferred

choice for both patients and medical professionals.

The effectiveness and

efficiency of this approach have not only provided hope and happiness to

countless individuals and families but have also significantly advanced the

field of fertility treatment. By continuously improving and refining the

techniques involved, fresh non-donor IVF cycles have set a new standard for

reproductive medicine, ensuring a brighter future for those seeking assisted

reproductive technologies.

End User Insights

Based on end

user, in 2024, the fertility clinics segment emerged as the dominant force in

the market, capturing the largest market share. This remarkable achievement can

be primarily attributed to the unprecedented global expansion of fertility

clinics, which have witnessed substantial growth in recent years. The

increasing awareness and acceptance of assisted reproductive technologies,

particularly in vitro fertilization (IVF), have played a pivotal role in

shaping consumers' decisions to pursue IVF treatment at these clinics.

The

availability of advanced reproductive technologies, such as preimplantation

genetic testing and embryo cryopreservation, has further enhanced the appeal of

fertility clinics. These cutting-edge techniques offer improved success rates

and higher chances of positive outcomes, instilling confidence in individuals

and couples seeking fertility treatments. With the continuous advancements in

medical research and technology, fertility clinics have become a beacon of hope

for those longing to start or expand their families.

As a

result, the demand for IVF services has been steadily increasing, propelling

the growth of fertility clinics worldwide. The comprehensive range of services

offered, including personalized treatment plans, state-of-the-art laboratory

facilities, and experienced medical professionals, further contribute to the

rising popularity of these clinics. With their unwavering commitment to patient

care and success, fertility clinics continue to revolutionize the field of

reproductive medicine and provide new opportunities for individuals and couples

striving to fulfill their dreams of parenthood.

Download Free Sample Report

Regional Insights

The

western region of India, particularly Maharashtra and Gujarat, is expected to

have a strong and influential presence in the Indian In-vitro Fertilization

(IVF) market. This dominance can be attributed to a combination of factors that

contribute to the region's remarkable growth in this field. One of the key

factors is the high per capita income in Maharashtra and Gujarat, which enables

a significant portion of the population to afford IVF procedures. This

financial capability, coupled with increasing awareness about the benefits and

success rates of IVF treatments, has led to a surge in demand for such

procedures in the region.

The western region is home to several reputable fertility clinics that have

established a strong reputation for providing high-quality IVF services. These

clinics offer state-of-the-art treatment facilities, advanced medical

technologies, and experienced fertility specialists who are dedicated to

helping couples achieve their dream of parenthood. Mumbai, the bustling

metropolis in Maharashtra, stands out as a hub for IVF centers, with a significant

number of clinics offering comprehensive and personalized treatment options. The

combination of these factors has created a favorable environment for the growth

of the Indian IVF market in the western region. As more individuals and couples

turn to IVF as a viable solution for their fertility challenges, the market is

poised for further expansion and advancements in the years to come.

Recent Development

- In March 2026, Nova IVF Fertility entered Kerala through the acquisition of Craft Fertility, with plans to open 10 new IVF centres across the state over the next three to five years. The reports described the move as Nova’s formal entry into Kerala and said the expansion would extend advanced reproductive services into urban as well as tier 2 and tier 3 locations, combining Nova’s scale with Craft’s long-standing regional clinical expertise. This was an important market development for India IVF because it reflected continuing consolidation by organized fertility chains and a push to widen access beyond the largest metro clusters.

- In February 2026, Mumbai’s KEM Hospital launched the MAA IVF Centre, a new state-of-the-art public-sector fertility unit created through a public-private partnership with former students Dr. Anjali and Dr. Aniruddha Malpani. News reports said the centre would provide IVF, intrauterine insemination, and intracytoplasmic sperm injection, while also expanding into embryo freezing, sperm and egg banking, research, and specialist training for gynecology residents. The development was significant because it brought advanced IVF capability back to the hospital where India’s first officially documented test-tube baby was born, while explicitly focusing on affordable and ethical fertility care within the public healthcare system.

- In December 2025, Intas Pharmaceuticals partnered with IntegriMedical to launch India’s first needle-free injection system for IVF and gynaecology treatments. The agreement gave Intas exclusive rights to deploy IntegriMedical’s proprietary technology in these therapy areas, with the stated goal of reducing pain, needle anxiety, and treatment fatigue for women undergoing repeated hormone injections during fertility care. This launch stood out in the IVF segment because it introduced a patient-experience innovation into a treatment pathway that typically requires a high volume of injections over multiple cycles.

- In May 2025, SpOvum Technologies and Khushi Fertility announced a collaboration to build AI-powered IVF infrastructure in India, combining technology development with clinic-level implementation. The partnership was structured so SpOvum would lead embryologist training and capacity building, while also embedding real-time R&D labs inside Khushi Fertility’s clinical environments to support faster validation and product development for the Indian IVF market. This was a notable collaboration because it went beyond a simple software deployment and aimed to standardize lab practices, improve monitoring, and raise treatment quality through a feedback-driven innovation model.

Key Market Players

• CK Birla Healthcare Pvt. Ltd.

• Nova IVF

• Indira IVF Hospital Private Limited.

• Apollo Fertility (Apollo Specialty Hospitals Pvt. Ltd.)

• Max Healthcare

• Manipal Health Enterprises Pvt. Ltd.

• Bloom Fertility Centre

• BACC Healthcare Private Limited

• Cloudnine Hospitals

• Morpheus IVF

• Babies and Us Fertility and IVF Centre (Ind) Pvt. Ltd.

|

By Technique

|

By Product

|

By Donor

|

By Infertility

|

By Embryo

|

By End User

|

By Region

|

- ICSI IVF

- Non-ICSI/ Traditional

IVF

|

- IVF Culture Media

- ICSI Machine

- IVF Incubators

- Cryosystem

- Others

|

- Fresh Non-donor

- Frozen Non-donor

- Fresh Donor

- Frozen Donor

|

|

- Fresh Embryo

- Frozen-thawed Embryo

|

- Fertility Clinics

- Hospitals

- Others

|

|

Report Scope:

In this report, the India In-vitro Fertilization

Market has been segmented into the following categories, in addition to the

industry trends which have also been detailed below:

- India In-vitro Fertilization

Market, By

Technique:

o ICSI IVF

o Non-ICSI/ Traditional IVF

- India In-vitro Fertilization

Market, By

Product:

o IVF Culture Media

o ICSI Machine

o IVF Incubators

o Cryosystem

o Others

- India In-vitro Fertilization

Market, By

Donor:

o Fresh Non-donor

o Frozen Non-donor

o Fresh Donor

o Frozen Donor

- India In-vitro Fertilization

Market, By InFertility:

o Male

o Female

- India In-vitro Fertilization

Market, By

Embryo:

o Fresh Embryo

o Frozen-thawed Embryo

- India In-vitro Fertilization

Market, By

End User:

o Fertility Clinics

o Hospitals

o Others

- India In-vitro Fertilization

Market, By

Region:

o North

o South

o West

o East

Competitive Landscape

Company Profiles: Detailed analysis of the major companies

present in the India In-vitro Fertilization Market.

Available Customizations:

India In-vitro Fertilization Market report with

the given market data, TechSci Research offers customizations according to a

company's specific needs. The following customization options are available for

the report:

Company Information

- Detailed analysis and

profiling of additional market players (up to five).

India In-vitro Fertilization Market is an upcoming

report to be released soon. If you wish an early delivery of this report or

want to confirm the date of release, please contact us at [email protected]